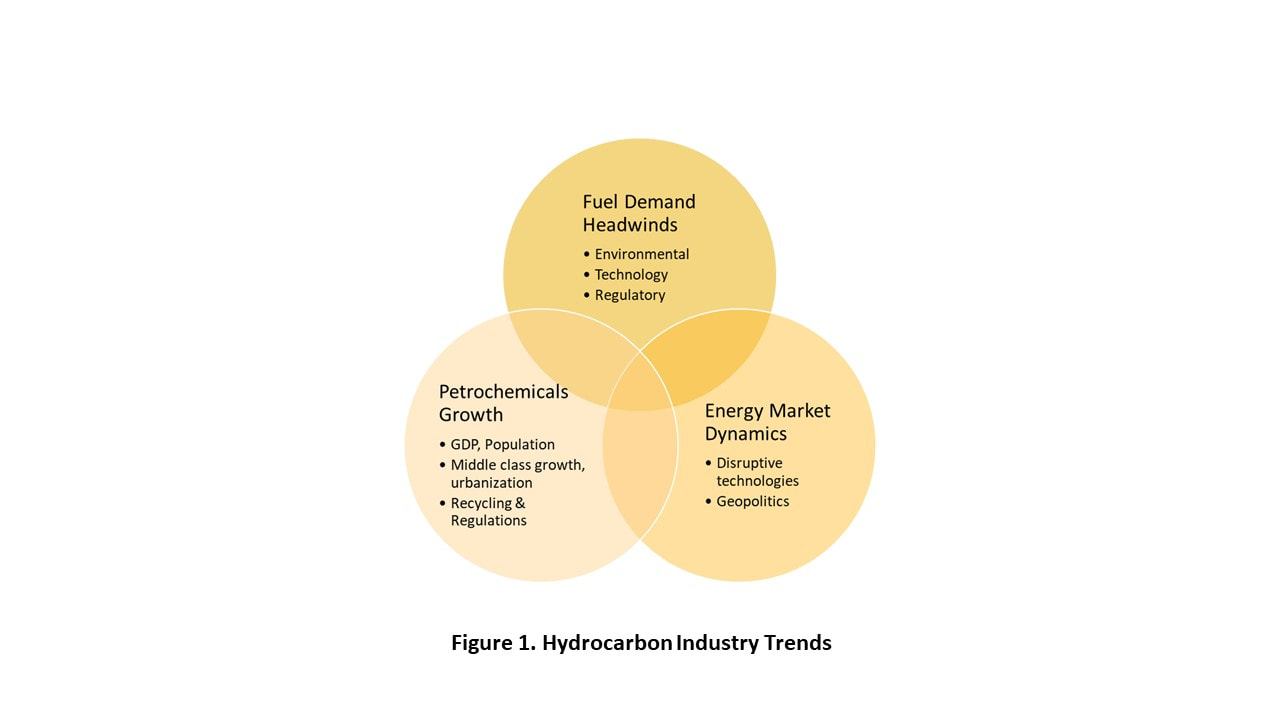

We expect a supply overhang in olefins industry in next two to three years, can be even sooner. Main factors contributing to this are:

Here are some of the smart ways to prepare for the future:

- Planned cracker capacity additions in North America, Asia including China, and Middle East

- Softening demand

- slowing economic growth

- Geopolitics – Middle East tensions, Tariffs/Trade barriers

Here are some of the smart ways to prepare for the future:

- Take a holistic view of the business

- Mid to long term targets for business growth

- Aligning current efforts with future growth expectations

- Utilizing the current assets effectively and efficiently

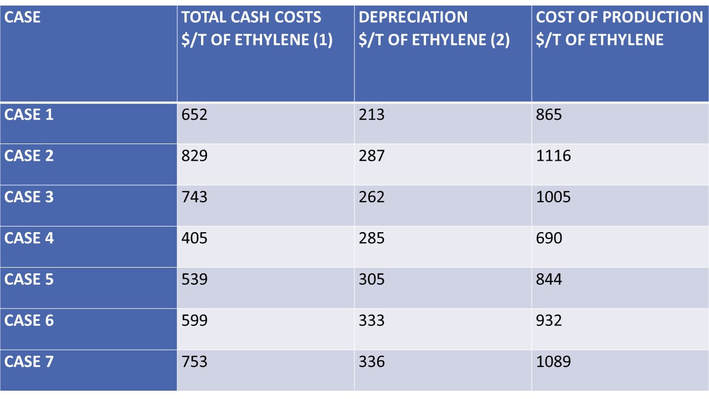

- Cost of production from your existing assets

- Current / historical operation and performance parameters along with benchmarks

RSS Feed

RSS Feed