The case study will highlight options for refinery/petrochemical integration and their impact on steam cracker economics.

The case study presented here is for the steam cracker with its associated utilities, storages etc. This study reviews cost of productions for six different levels of refinery-petrochemical integration. For reference, a purity ethane cracking case is added. All cases were studied for a 1,200 kTA steam cracker located in Asia. The energy and feed/product pricing are based on crude oil at $75 per barrel and natural gas $6 per million Btu.

The cases are described below:

Case 1: Ethane cracking, mostly based on imported feed supply

Case 2: Naphtha Cracking based on different naphthas from the refinery

Case 3: Ethane and High severity FCC off gas based on import ethane and large capacity high olefins mode of FCC operation in refinery

Case 4: FCC off gases, Coker off gases, saturated gases based on large and complex refinery with FCC, Delayed Cokers, Platforming/Aromatics, Hydrotreating/Hydro-processing units that generate large amount of off gases. In this refinery fuel demand is met by import of fuel gas or through synthetic fuel gas generation (like coke gasification).

Case 5: Heavy naphtha and hydrotreated vacuum gas oil feed based on medium complexity refinery with heavy crudes

Case 6: Naphtha, Light/heavy gas oils, Hydrocracker distillate, butane, refinery off gases based on a complex refinery with hydrocracking/hydrotreating, FCC and Platforming units. High level of integration and optimization based on crude diet to the refinery.

Case 7: Light crude (OSO) cracking based on the concept of minimum processing/separation of unprocessed crude sources

Refinery off gas stream typically contain contaminants that impact the product quality and ethylene plant operation. These contaminants need to be pretreated to ensure reliable and safe operation of the steam cracker. Steam cracker design must account for variations and flexibility of feedstock due to changes in crude oils handled in the refinery and the normal adjustments made in the refinery processing to meet changing fuels demand. Evaluation and selection of design options to optimize an integrated complex requires a great deal of understanding about refinery operations as well as the steam cracker design, operation and reliability. The decisions made during early stages of facility development have a major impact on the overall economics over the life of that facility and therefore the competitiveness. Hydrocarbon management is the key to convert the synergy of refinery-petrochemicals operation into an economic advantage in a market place of constantly changing energy dynamics and shifting product demands. Therefore, the optimization should be based on the integrated facility level depending on supply/demand and pricing of raw materials and products at the in/out boundary. Any sub-optimization based on artificially fixed transfer pricing defeats the purpose of integration synergies.

For this case study, the process units include feed preparation and treating as required. Mixed C4s and Raw Pygas are sent to downstream units for further processing. Main by-products include hydrogen, polymer grade propylene, mixed C4s and raw pygas. In addition, gas oil and fuel oil products are routed to other facilities.

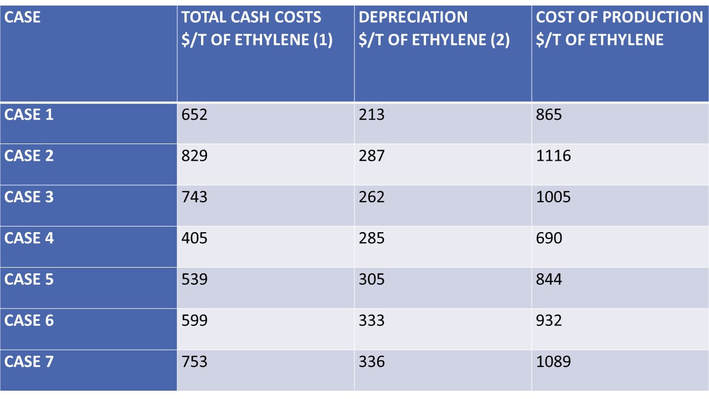

The table below summarizes the cost of production for all cases based on grassroots facility:

(1) Total cash costs include cost of raw materials, credits for by-products, utility costs and fixed (labor costs, overheads, maintenance, insurances/property tax etc.) costs.

(2) Depreciation is based on capital costs for ISBL and OSBL facilities as well as owner’s costs during development and execution of the project.

The overall economics is dependent on feed, product and energy pricing. The table above presents a snapshot cost of production for different options for refinery-petrochemical integration. This analysis provides relative comparison of integration options and their impact on cracker economics based on historic prices of cracker feeds relative to crude pricing (therefore these do not represent a true indication of synergy advantages of integrated operation). For this pricing scenario, the refinery off-gas based cracker (Case 4) results in lowest cost of production. It also indicates that the higher levels of integration provide the opportunities to improve cracker economics as compared to a conventional naphtha cracker (Case 2).

The integrated complexes will have a better economic return and diversified market as compared to standalone fuels refineries. Steam crackers in crude oil feed dependent regions must compete with feed advantaged regions (like North America’s shale-based ethane or Middle East’s low-priced feedstock) and look for feedstock supply integration and synergies.

The case study presented here is for the steam cracker with its associated utilities, storages etc. This study reviews cost of productions for six different levels of refinery-petrochemical integration. For reference, a purity ethane cracking case is added. All cases were studied for a 1,200 kTA steam cracker located in Asia. The energy and feed/product pricing are based on crude oil at $75 per barrel and natural gas $6 per million Btu.

The cases are described below:

Case 1: Ethane cracking, mostly based on imported feed supply

Case 2: Naphtha Cracking based on different naphthas from the refinery

Case 3: Ethane and High severity FCC off gas based on import ethane and large capacity high olefins mode of FCC operation in refinery

Case 4: FCC off gases, Coker off gases, saturated gases based on large and complex refinery with FCC, Delayed Cokers, Platforming/Aromatics, Hydrotreating/Hydro-processing units that generate large amount of off gases. In this refinery fuel demand is met by import of fuel gas or through synthetic fuel gas generation (like coke gasification).

Case 5: Heavy naphtha and hydrotreated vacuum gas oil feed based on medium complexity refinery with heavy crudes

Case 6: Naphtha, Light/heavy gas oils, Hydrocracker distillate, butane, refinery off gases based on a complex refinery with hydrocracking/hydrotreating, FCC and Platforming units. High level of integration and optimization based on crude diet to the refinery.

Case 7: Light crude (OSO) cracking based on the concept of minimum processing/separation of unprocessed crude sources

Refinery off gas stream typically contain contaminants that impact the product quality and ethylene plant operation. These contaminants need to be pretreated to ensure reliable and safe operation of the steam cracker. Steam cracker design must account for variations and flexibility of feedstock due to changes in crude oils handled in the refinery and the normal adjustments made in the refinery processing to meet changing fuels demand. Evaluation and selection of design options to optimize an integrated complex requires a great deal of understanding about refinery operations as well as the steam cracker design, operation and reliability. The decisions made during early stages of facility development have a major impact on the overall economics over the life of that facility and therefore the competitiveness. Hydrocarbon management is the key to convert the synergy of refinery-petrochemicals operation into an economic advantage in a market place of constantly changing energy dynamics and shifting product demands. Therefore, the optimization should be based on the integrated facility level depending on supply/demand and pricing of raw materials and products at the in/out boundary. Any sub-optimization based on artificially fixed transfer pricing defeats the purpose of integration synergies.

For this case study, the process units include feed preparation and treating as required. Mixed C4s and Raw Pygas are sent to downstream units for further processing. Main by-products include hydrogen, polymer grade propylene, mixed C4s and raw pygas. In addition, gas oil and fuel oil products are routed to other facilities.

The table below summarizes the cost of production for all cases based on grassroots facility:

(1) Total cash costs include cost of raw materials, credits for by-products, utility costs and fixed (labor costs, overheads, maintenance, insurances/property tax etc.) costs.

(2) Depreciation is based on capital costs for ISBL and OSBL facilities as well as owner’s costs during development and execution of the project.

The overall economics is dependent on feed, product and energy pricing. The table above presents a snapshot cost of production for different options for refinery-petrochemical integration. This analysis provides relative comparison of integration options and their impact on cracker economics based on historic prices of cracker feeds relative to crude pricing (therefore these do not represent a true indication of synergy advantages of integrated operation). For this pricing scenario, the refinery off-gas based cracker (Case 4) results in lowest cost of production. It also indicates that the higher levels of integration provide the opportunities to improve cracker economics as compared to a conventional naphtha cracker (Case 2).

The integrated complexes will have a better economic return and diversified market as compared to standalone fuels refineries. Steam crackers in crude oil feed dependent regions must compete with feed advantaged regions (like North America’s shale-based ethane or Middle East’s low-priced feedstock) and look for feedstock supply integration and synergies.

RSS Feed

RSS Feed