This question is on the minds of crude oil suppliers and refiners for developing a sustainable business strategy. Many consulting and forecasting pundits believe that crude oil demand will peak sometime between 2030 to 2040. This challenge is different than the crude supply constraints that the world was expected to run out of crude oil/hydrocarbons and was on everyone’s mind in previous decades. The concern now is that with abundant crude resources and declining demand can threaten the industry’s future. Businesses hope and expect that the demand for hydrocarbons for petrochemicals will grow at a higher pace (in-line with GDP growth) and can be an answer to the business sustenance. “Are Petrochemicals the answer to Crude Oil Demand?” is a key question that most of the companies in oil and gas businesses are trying to fully understand. We think that petrochemicals are going to be a part of the answer in the short to mid-term and that there is greater uncertainty about the long-term future. Multiple trends are at play and more are expected to evolve, which will influence the future.

Yes, Petrochemicals are part of the answer – Business Case

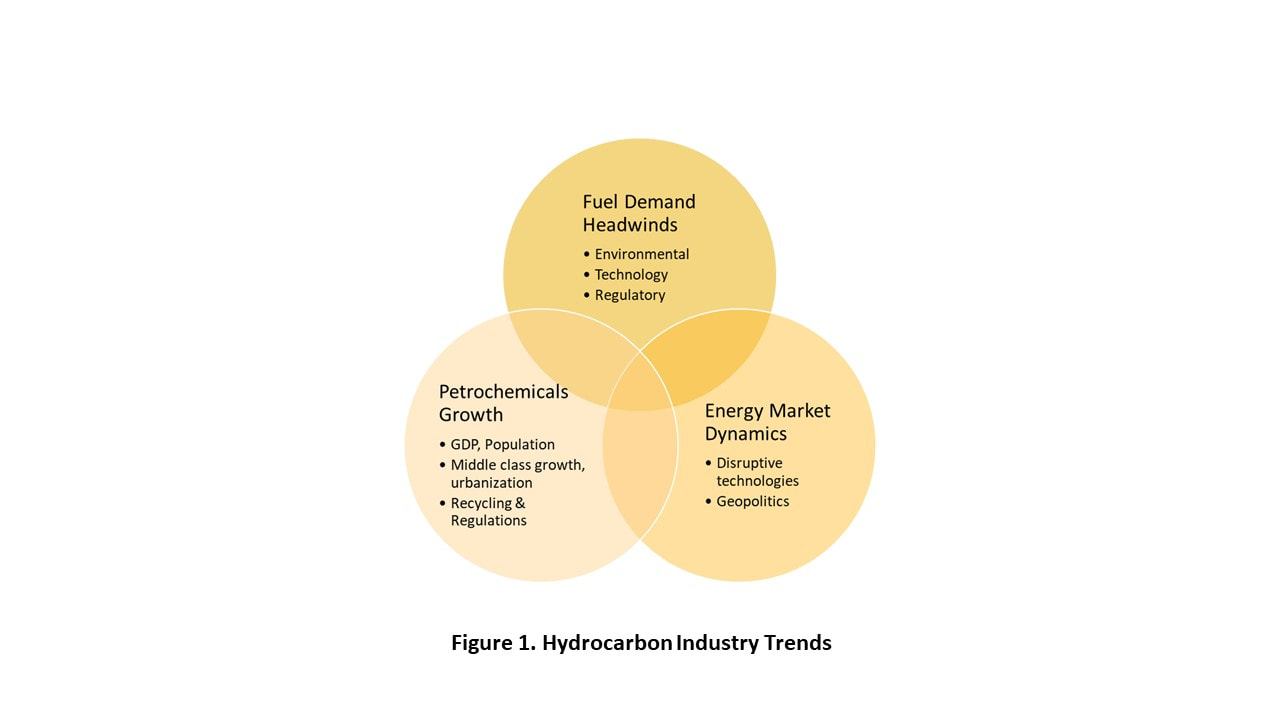

Figure 1 highlights some of the current industry trends that are shaping the future. Fuel demand, particularly in the transportation sector, is facing environmental pressure due to climate change (including greenhouse gas emissions) and air quality in large urban centers. Electrification of vehicles, sharing platforms (like Uber, etc.), and disruptive technologies/models for supply chains including commercial transportation (mainly trucks and freight carriers) will impact fuel demand significantly in coming years. The regulatory environment is evolving quickly to limit emission levels related to sulfur and other components as well as requiring electrification of transportation systems and higher contribution of renewable/alternate energy sources. These forces will result in a slowdown in fuel demand in the coming years.

The energy market has always been very dynamic over the last 50 years driven mostly by geopolitics along with demand growth in developing economies. The last decade has seen disruptive technologies, particularly shale, playing a much larger role in shaping the energy market. These resulted in higher market volatility. Geopolitics has been further complicated by sanctions regime and threats of trade barriers/tariffs. Countries around the world are rethinking their energy security and options to lower current threats and risks.

Hydrocarbon demand for the petrochemical industry is expected to grow at much higher levels as compared to energy demand. Petrochemicals demand is closely tied to the growth of GDP and population growth. It’s driven primarily by the growing middle class in emerging economies and a larger shift of population to urban centers. Petrochemical growth will see some negative impacts due to changes in the regulatory environment (e.g. ban on single-use plastics) and a greater emphasis as well as environmental pressure for increased plastic recovery and recycling. Overall petrochemical products contribute tremendously to improving quality of life and as a larger percentage of the population in developing economies move into the middle class, we will see continued growth in demand.

It’s no surprise that refineries are now looking at higher levels of petrochemical integration as a prudent diversification strategy for future sustainable growth. This is evident from some of the complexes that are currently in engineering and construction or in the early stages of development. Some of the recent announcements include:

I will touch some more on refinery-petrochemical integration in the future. Please feel free to contact me at [email protected]

Yes, Petrochemicals are part of the answer – Business Case

Figure 1 highlights some of the current industry trends that are shaping the future. Fuel demand, particularly in the transportation sector, is facing environmental pressure due to climate change (including greenhouse gas emissions) and air quality in large urban centers. Electrification of vehicles, sharing platforms (like Uber, etc.), and disruptive technologies/models for supply chains including commercial transportation (mainly trucks and freight carriers) will impact fuel demand significantly in coming years. The regulatory environment is evolving quickly to limit emission levels related to sulfur and other components as well as requiring electrification of transportation systems and higher contribution of renewable/alternate energy sources. These forces will result in a slowdown in fuel demand in the coming years.

The energy market has always been very dynamic over the last 50 years driven mostly by geopolitics along with demand growth in developing economies. The last decade has seen disruptive technologies, particularly shale, playing a much larger role in shaping the energy market. These resulted in higher market volatility. Geopolitics has been further complicated by sanctions regime and threats of trade barriers/tariffs. Countries around the world are rethinking their energy security and options to lower current threats and risks.

Hydrocarbon demand for the petrochemical industry is expected to grow at much higher levels as compared to energy demand. Petrochemicals demand is closely tied to the growth of GDP and population growth. It’s driven primarily by the growing middle class in emerging economies and a larger shift of population to urban centers. Petrochemical growth will see some negative impacts due to changes in the regulatory environment (e.g. ban on single-use plastics) and a greater emphasis as well as environmental pressure for increased plastic recovery and recycling. Overall petrochemical products contribute tremendously to improving quality of life and as a larger percentage of the population in developing economies move into the middle class, we will see continued growth in demand.

It’s no surprise that refineries are now looking at higher levels of petrochemical integration as a prudent diversification strategy for future sustainable growth. This is evident from some of the complexes that are currently in engineering and construction or in the early stages of development. Some of the recent announcements include:

- Saudi Aramco and SABIC JV for Crude Oil to Chemicals (COTC)

- Ratnagiri integrated Refinery and Petrochemical Complex (likely JV of 3 Indian Oil Companies, Saudi Aramco and ADNOC)

- DUQM Refinery and Petrochemical Integrated Project

- ADNOC Mixed Feed Cracker integrated with Refinery

- TOTAL, Saudi Aramco JV SATORP Mixed Feed Cracker integrated with the refinery

- 5 (or more) major Refinery-Petrochemicals integrated projects in China announced in the last 2 years

- Petronas and Saudi Aramco JV Refinery and Petrochemical integrated development (RAPID project)

I will touch some more on refinery-petrochemical integration in the future. Please feel free to contact me at [email protected]

RSS Feed

RSS Feed